Electric Batteries and Supply Chain Economics →

One of the many issues the global pandemic has exposed is the (mostly) single point of failure in global supply chain systems. Over the last couple of decades global corporations optimized their supply chain to such an extent that it became far from flexible, while being extremely optimized. While the supply chain disruptions in today’s products - from face masks to medical equipments got exposed, this post is about the future supply chain challenges.

With many countries rallying towards fighting climate change, electric vehicles are at the forefront of that fight. With the cost per kilowatt-hour touching $100/kWhr or even less, electric vehicles would not only make economic sense but also reduce the total cost of ownership drastically. While American companies like Tesla are at the head of the pack in innovation and execution, the components for uninterrupted production as well as security lie elsewhere - the supply chain for electric car batteries.

As Benchmark’s Simon Mores says there are two ways of reducing cost of Li-ion batteries:

- Controlling the supply of raw materials that go into batteries

- Changing how batteries are made (scale)

While the prices of raw materials were at all time high, companies like Tesla maintain lead by controlling the manufacturing process - “the scale” as 25-40% of the cost of an electric vehicle can be attributed to the cost of the battery. That is where Gigafactories become interesting and so does controlling the supply chain. But so far, American auto companies, to a large extent, have only been assembling the components that constitute the battery. There is a lot of effort that goes into a battery before this final assembly.

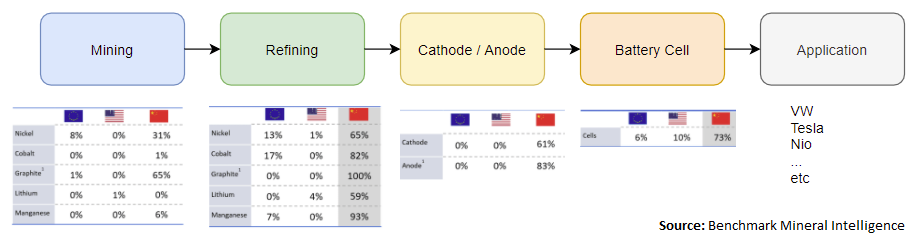

Let us break this apart looking at the value chain of electric battery manufacturing:

If one were to superimpose the geographies that control different parts of the value chain, one could immediately see the premonitions of future supply chain challenges.

More than 50% of every one of the raw materials is dependent on one geography, which is a recipe for future disruptions. As Benchmark’s Vivas Kumar points out, the only part of the value chain that can’t be moved around are the mines themselves. Every other part of the value chain can be located in different parts of the globe. Most of the early stages of the value chain like Cathode, cell manufacturing, etc. are controlled predominantly by specific geographies that would be a supply chain and security risk when electric vehicles become like mobile phones. A wise thing for such an industry like Auto to do is to shore up the different components so that the critical component (battery) supply is not disrupted in the future.

One has to wait and see if the electric battery supply chain gets reshored and does not become another disruption waiting to happen or if short term optimization goals will lead to long-term disasters, just as it is happening in semiconductors and electronics.